„What Gets Measured Gets Financed“ , says a report by The Rockefeller Foundation and Boston Consulting Group form November 2022 and finds that a lack of complete and comparable data—especially about private sector climate finance—hinders efforts to close the existing finance gaps. The report captures capital need in the real economy and actual capital flows for mitigation, adaptation and resilience.

The report suggests that the capital currently deployed provides only about 16% of the total climate finance required to mitigate negative climate effects and adapt processes and infrastructure worldwide. At the same time, the report states that

- there is no consensus on how to measure and report climate finance;

- data is poorly measured and tracked across climate finance today;

- improved data can drive climate finance.

„The buildings sector has the second-largest mitigation finance need after the power sector, at just over $660 billion per year from 2020 to 2025. But as of 2020, flows stood at just $260 billion. (…) Even so, long payback periods and the different incentives offered to building owners and tenants have discouraged financing and investment in decarbonization. Continued policy support is essential to increasing investment—especially in light of the high upfront costs associated with many decarbonization levers such as full-building envelope retrofits.“

The Rockefeller Foundation / Boston Consulting Group, Climate Finance Funding Flows and Opportunities, What Gets Measured Gets Financed, November 2022, p. 24

To close the financing gap, the climate finance community requires more data on where proceeds are being deployed. A strong disclosure framework based on a common set of taxonomies and reporting mandates— including provisions for proprietary data – is seen as beeing able to facilitate greater data transparency. According to the report, all key participants in the climate finance ecosystem have to improve the quality, consistency, and frequency of their reporting.

While the Taskforce for Climate-related Financial Disclosures (TCFD) has been a major driver of action in measuring and integrating climate risks throughout business operations and investment portfolios, the Taskforce on Nature-related Financial Disclosures (TNFD) is working to develop and deliver a risk management and disclosure framework for organisations to report and act on evolving nature-related risks, with the ultimate aim of supporting a shift in global financial flows away from nature-negative outcomes and toward nature-positive outcomes.

According to the TNFD, better information will allow financial institutions and companies to incorporate nature-related risks and opportunities into their strategic planning, risk management and asset allocation decisions.

In November 2022, TNFD released the third version of its beta framework for market consultation. The next version of the beta framework will be released in March 2023 (v0.4), before the release of version v1.0 of the full framework for market adoption in September 2023.

TCFD, Implementing the Recommendations of the Task Force on Climate-related Financial Disclosures, 2021

- Rechtskonforme ESG/CSR-Berichte: Neue Leitlinien, Leitfäden, Empfehlungen & Standards für das Nachhaltigkeits-Reporting

- Sustainable Finance Strategy on track: Neues zur EU-Taxonomie, Offenlegungsverordnung und nationalen Nachhaltigkeitsstrategie

- Deutscher Corporate Governance Kodex (DCGK) 2022 und EU Corporate Sustainability Reporting Directive (CSRD): Nachhaltigkeit nach innen und nach außen

In Germany, the federal government has defined the approach of sustainable finance as a powerful lever for transformation in the economy in its current policy statement 2022 on the German Sustainability Strategy and has set itself the goal of developing Germany into no less than the leading location for sustainable finance. It welcomes the establishment of the International Sustainable Standards Board in Frankfurt / Main, which is of great importance for Germany as a location for sustainable finance.

IN DEPTH: IFRS Sustainability Standards Board (ISSB)

On 3 November 2021, the IFRS Foundation Trustees announced the creation of a new standard-setting board—the International Sustainability Standards Board (ISSB)—to help meet the demand for high quality, transparent, reliable and comparable reporting by companies on climate and other environmental, social and governance (ESG) matters. The intention is for the ISSB to deliver a comprehensive global baseline of sustainability-related disclosure standards that provide investors and other capital market participants with information about companies’ sustainability-related risks and opportunities to help them make informed decisions.

To evolve from the currently fragmented ESG disclosure landscape, that lacks connectivity and has conflicting concepts, to a truly global common language of sustainability-related financial disclosures, the ISSB agreed during recent meetings ahead of the publication of the IFRS Sustainability Disclosure Standards in 2023 that it would be beneficial to ground its standard-setting work by clearly articulating the relationship between sustainability matters and financial value creation.

In its session on 13 December 2022, the ISSB agreed how to describe sustainability and clarified that a company’s ability to deliver value for its investors is inextricably linked to the stakeholders it works with and serves, the society it operates in, and the natural resources it draws on. The decision builds on concepts from the Integrated Reporting Framework, which helps companies articulate how they use and effect resources and relationships for creating, preserving and eroding value over time.

Sustainability will be described in the ISSB’s General Sustainability-related Disclosures Standard as the ability for a company to sustainably maintain resources and relationships with and manage its dependencies and impacts within its whole business ecosystem over the short, medium and long term. Sustainability is a condition for a company to access over time the resources and relationships needed (such as financial, human, and natural), ensuring their proper preservation, development and regeneration, to achieve its goals.

By referring to this articulation of the value creation process, a company will be better placed to explain to its investors how it is working sustainably within its business ecosystem—addressing the impacts, risks and opportunities that can affect its performance and prospects—to ultimately deliver financial value for investors.

IFRS, ISSB describes the concept of sustainability and its articulation with financial value creation, and announces plans to advance work on natural ecosystems and just transition, December 2022

The German Federal Government is supported by the Sustainable Finance Advisory Committee (Sustainable Finance-Beirat) in ambitiously implementing and further developing the Sustainable Finance Strategy. According to the Sustainable Finance Advisory Committee, robust, verifiable and comparable sustainability information is the basis for an active and effective approach to sustainability issues in the financial sector. It supports the current standard development at European (EFRAG) and global level (ISSB and GRI) and promotes their close coordination and harmonisation for the sake of effective and consistent impact. The Commitee fully supports the ISSB’s ambition to develop a global baseline for sustainability reporting considering the investor focus on enterprise value, highly welcome the agreement between the ISSB and the Global Reporting Initiative (GRI) to coordinate their programmes and standard-setting activities and provides full support to the efforts of standard setters and regulators in harmonizing, aligning and standardizing the requirements for integrated corporate sustainability reporting.

After the first set of ESRS are handed over by EFRAG, we ask the EC to start a due process with the objective of ensuring full interoperability between European sustainable finance regulations including the Sustainable Finance Disclosure Regulation (SFDR), CSRD, Taxonomy regulation, and Corporate Sustainability Due Diligence Directive (CSDDD); in addition the ESRS standards need to be harmonized as much as possible at the intersection with the ISSB and GRI standards.

The Sustainable Finance Advisory Committee, Open Letter on Sustainability Reporting, October 31th, 2022

Meanwhile, according to the KfW Climate Barometer 2022 (KfW-Klimabarometer 2022), which surveyed climate protection investments by the entire corporate sector in Germany for the first time, only slightly more than one third of all companies (37 %) rate the transformation to sustainability-oriented financial markets as important or very important policy measures to support climate protection investments. In contrast, almost two-thirds of all companies (64 %) consider the simplification of planning and approval procedures to be an important goal, and just under half even consider this to be a very important goal (45 %). The call for subsidies ranks second in importance (59 %). In third place comes greater planning certainty with regard to the GHG / CO2 price (56 %).

IN DEPTH: Real Estate

By comparison, a review of the TCFD disclosures of BBP members in 2022 found that the market response to climate change is expected to impact real estate companies in several ways: Increasing regulation of energy and carbon in buildings and supply chains, changing occupier and investor preferences and increasing requirements around ESG and sustainability in order to access finance (BBP, A Guide to Climate Resilience Strategies for Commercial Real Estate, 2022).

A current survey conducted by Berlin Hyp as part of its regular trend barometer (Trendbarometer-Umfrage der Berlin Hyp) has revealed for the German commercial real estate market, among other things, that the reluctance of real estate financiers to provide financing means that the quality and future viability of real estate projects will be more important than ever, while after the interest rate trend and the price trend for real estate, the cost expectation for properties that have not been optimised in terms of energy efficiency is rated as a major challenge for real estate investors. Mirroring this, the megatrend ecology will be the determining factor for 86% of the survey participants in the next 24 months, followed by the megatrend digitalisation with 71%.

This is in line with the PwC/ULI study Emerging Trends in Real Estate Europe 2023, according to which the environmental criterion in the ESG approach has become fundamental for investment success and that new energy infrastructures (solar and wind energy, energy storage, electric transport infrastructure, etc.) top the ranking of the top sectors. The focus on ESG is expected to be the most impactful trend over the next 20 years.

Pursuant to the KfW Climate Barometer, only around 15 % of companies assume in each case that customers demand at least a partial contribution from them to climate protection or that climate protection is an important topic in financing discussions. Accordingly, only 5 % of the companies stated that the EU’s Taxonomy Regulation for Sustainable Business is relevant for their own company. However, this is an average view that is strongly driven by the high number of small companies in Germany. Among large companies, 88 or 67 % of the companies are confronted with corresponding requirements by customers or financing partners.

In the increasingly sustainability-oriented regulatory environment, it is becoming more and more important for companies of all sizes to have detailed and reliable information on the effects of their business activities on the environment and society and, conversely, how climate risks affect business development.

KfW-Klimabarometer 2022

IN DEPTH: Risk Management & Climate Stress Tests

Even if this has not yet reached many German companies, the KfW Climate Barometer is right in pointing to an increasingly sustainability-oriented regulatory environment. This is true not least because of the amendment to the Minimum Requirements for Risk Management (MaRisk), which will be finalised and come into force in 2023. The Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufsicht, BaFin) has already submitted an amended draft of its letter „Minimum Requirements for Risk Management“ („Mindestanforderungen an das Risikomanagement“, MaRisk) for consultation. The primary objective of the seventh amendment to MaRisk is to implement the guidelines of the European Banking Authority (EBA) for lending and monitoring. In addition, requirements for the management of sustainability risks are included for the first time. In addition, the amendment takes up findings from the audit practice on the institutions‘ own real estate transactions.

For the purposes of this BaFin letter, ESG risks are events or conditions in the environmental, social or corporate governance fields. The occurrence of such events or conditions may have a potentially negative impact on the net assets, financial position or results of operations of a supervised entity. In this respect, ESG risks act as risk drivers and can have an impact on credit risks (including country risks), market price risks, liquidity risks and operational risks as well as other material risk types.

Consequently, a position paper of the Bundesverband deutscher Banken e. V. (Association of German Banks) on the implementation of climate stress tests in risk management of December 2022 (Implementierung von Klimastresstests im Risikomanagement) recommends treating ESG risks as a risk driver that affects the established risk types (credit risk, market price risk, etc.). At the same time, however, it is also stated here that in the context of climate and environmental risks, the data situation is currently anything but favourable, which is why the most important exercise would first be to create a good data basis.

The banking association divides climate and environmental risks into physical and transitory risks and understands them as drivers for already existing risk types. For the construction and real estate sector in particular, the Bankers Association explicitly addresses credit risks (counterparty risks), strategic risks, reputational risks, operational risks including climate-related legal risks, liquidity risks, market price risks and residual value risks. For residential real estate, the banking association initially focuses on risk concentration due to the employer’s sector, and for commercial real estate on transitory risks.

The KfW Climate Barometer survey assumes that the goal of climate neutrality requires extensive investments in all sectors of the economy. In order to achieve the goal of climate neutrality in Germany, companies will have to invest an average of around EUR 120 billion annually by 2045. Economic efficiency is rated by companies as the most important decision factor for or against a climate protection investment. Reliable framework conditions and clear financial incentives are the key levers for enabling the upcoming investments. Across all company sizes, the KfW Climate Barometer identifies a strong correlation between (perceived) stakeholder pressure and companies‘ commitment to climate protection: When companies face pressure from their customers, their financing partners or regulation, they are more likely to have climate protection embedded in their corporate strategy, to have formulated GHG reduction targets for their company and to be aware of their GHG footprint.

In 2021, around 870,000 companies are expected to have invested a total of €55 billion in projects that also serve climate protection. This corresponds to 23 % of all companies in Germany.

- Most frequently, companies that have made climate-related investments have implemented measures in the area of climate-friendly mobility (e.g. acquisition of an electric car or corresponding charging infrastructure, 47 %).

- About one third of the investing companies (32%) have made investments to improve the energy efficiency of existing buildings (e.g. through thermal insulation or the installation of heat pumps).

- Third place is taken by measures to generate or store electricity or heat from renewable energies (27%).

- Energy efficiency measures in newly constructed buildings and measures to improve energy efficiency in process or plant technology (e.g. production, cooling) each have a frequency of 12 %.

Reducing energy costs is the first motive for companies to invest in climate protection. The second most common motive for companies that have already made climate protection investments is their own contribution to climate protection, followed by compliance with legal requirements. The reasons that follow are the use of public funding and customer requirements. The development of new sales markets and the avoidance of reputational risks, on the other hand, currently play a surprisingly subordinate role in the broad spectrum of companies.

If German companies succeed in providing technical solutions for achieving the ambitious global emission reduction targets, this can increase value creation, employment and prosperity in Germany and at the same time make a significant contribution to climate protection worldwide.

KfW-Klimabarometer 2022

A German real estate industry initiative with the self-designation ESG Circle of Real Estate (ECORE) presented a label for more transparency in the sustainability performance of real estate portfolios in December 2022. In addition to the portfolio approach, another innovation shall be relevant in the context of financing: With an ECORE Finance Score, financial institutions shall be able to check the ESG compliance of the properties and the applicant in the context of financing requests and track the transformation process over the term of the financing. Beyond the ESG criteria, the required taxonomy criteria of the EU and the goals of the Paris Climate Agreement are to be mapped.

Fit für den Klimawandel? gif veröffentlicht Kennzahlenkatalog Immobilien-Risikomanagement – ohne Klimarisiken

Nachhaltigkeit, Klimaschutz und Risikosteuerung in Unternehmen: Vom CSR-Preisträger aus der Immobilienwirtschaft zum Management-Leitfaden für die Praxis

Klimaangepasstes Bauen, Arbeiten und Betreiben? Wie Extremwetter-Ereignisse Wertschöpfungs-Ketten beeinflussen

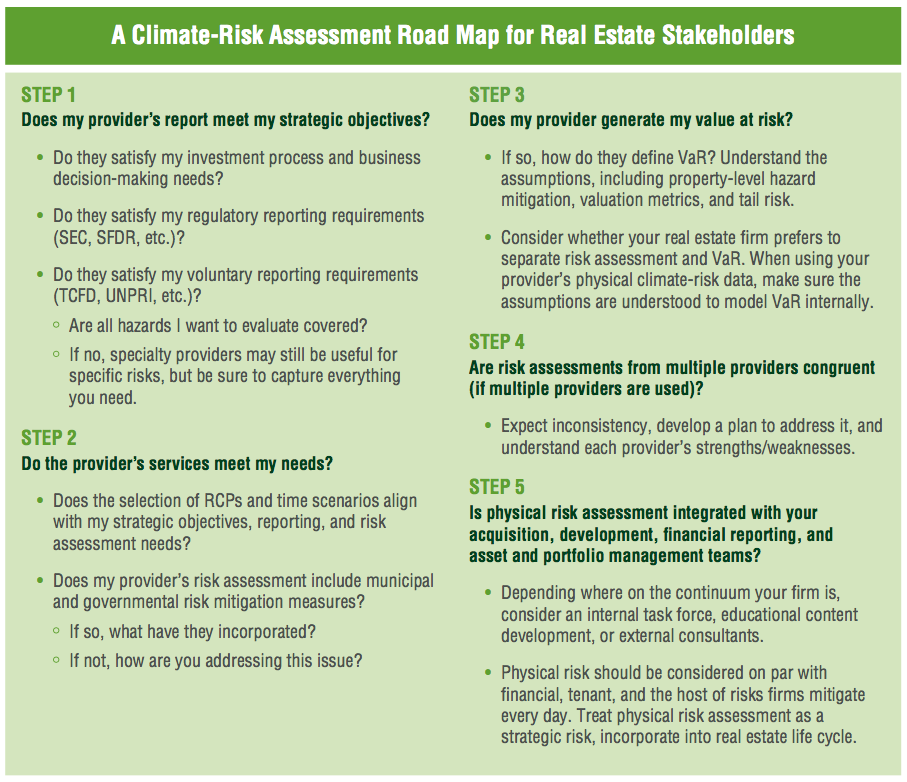

According to the ULI / LaSalle report How to Choose, Use, and Better Understand Climate-Risk Analytics the industry needs better models and better tools to better assess, price, and mitigate long-term climate risk in real estate.

The goal for real estate experts should be to understand the key inputs and how those might impact decision-making. Institutional real estate managers face the substantial challenge of translating complex climate models into real estate investment decisions, to interpret climate-risk analytics, identify risks effectively, and incorporate them in their decision-making throughout the investment life cycle. The next steps shall include the development of industry standards.

Thereby the report states, that institutional real estate managers would do well to carefully articulate their use case needs—specifically regarding valuation and value at risk. In that sense, during the period when the real estate industry develops standardized and industry-accepted practices, tools like the climate-risk assessment road map described adjacent could help to make more informed decisions.

The real estate industry can be a leader in this discussion, and in so doing needs to consider the broader goals.

Urban Land Institute. How to Choose, Use, and Better Understand Climate-Risk Analytics. Washington, DC: Urban Land Institute, 2022

The companies finding the most success on their climate journeys aren’t interested in basic compliance or achieving incremental improvements. They’ve embraced sustainability as a powerful business opportunity, embedding it into the core of their strategy.

BCG, Closing the Climate Action Gap, January 2023

© Copyright by Dr. Elmar Bickert

Du muss angemeldet sein, um einen Kommentar zu veröffentlichen.